You’ve probably heard it before — a friend or coworker proudly says, “My investments are up 20% this year!” It’s a common talking point. And while it’s exciting to see positive growth, it’s also where a dangerous myth in retirement planning begins: the average rate of return.

Many investors — especially those nearing retirement — believe their average return tells them everything they need to know about their financial future. But the truth is, this number can be misleading — and in some cases, provide a false sense of security just when you need real clarity the most.

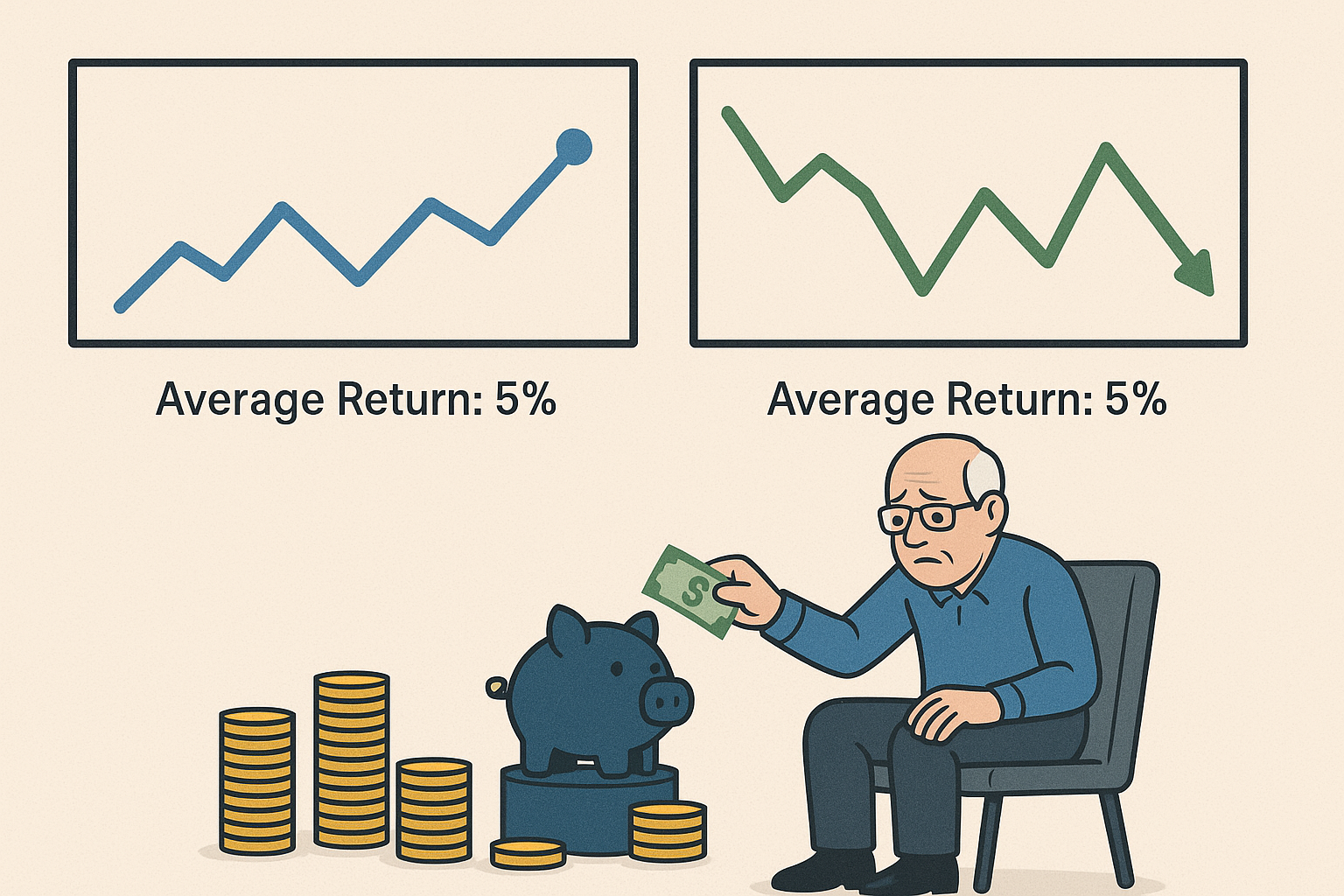

What Is Average Rate of Return?

The average rate of return is simply the mathematical average of gains and losses over a period of time. You’ll find it on 401(k) statements, performance reports, and marketing materials.

But here’s the key issue: you don’t retire on an average — you retire on what’s actually left. And average returns don’t account for sequence of returns risk, volatility, or withdrawals, which all matter deeply in retirement.

A Simple Example That Exposes the Risk

Let’s say you start with $100,000. Over four years, your returns look like this:

Year 1: +100% → $200,000

Year 2: -50% → $100,000

Year 3: +100% → $200,000

Year 4: -50% → $100,000

Your average return is +25% per year — but your account value is exactly where it started. That’s not growth. That’s a rollercoaster.

This illustrates a critical reality: you can have great average returns and still make no progress — or worse, lose ground — especially once you start drawing income.

Why This Matters More in Retirement

Before retirement, volatility is frustrating — but manageable. You’re contributing regularly and have time to recover from losses.

But once you start withdrawing from your accounts, the sequence of returns becomes incredibly important. A bad year early in retirement — especially while pulling income — can permanently reduce your portfolio’s ability to recover. You may be forced to sell investments at a loss, locking in damage that future growth can’t undo.

Two retirees could experience the same average return but end up with dramatically different outcomes depending on when those returns occur.

What We See in Real Life

At Financial Services of America, we’ve worked with thousands of individuals and couples transitioning into retirement. One common theme we see:

“Our portfolio has averaged 9-10% per year, so we feel good about where we’re at.”

But after a risk analysis, many are surprised to learn they’re carrying much more volatility than they realize — often in the 70–80 risk score range (on a 0–100 scale).

Without a distribution plan, they’re exposed to unnecessary risk that could jeopardize their income — just when they need it most.

A Better Way to Measure Retirement Readiness

Rather than focusing on average returns, ask yourself:

How much income can my savings reliably generate?

How would a market downturn affect my ability to retire confidently?

How protected am I against inflation, taxes, and healthcare costs?

What Matters More Than Average Returns

Here are five more relevant metrics to track instead of “average return”:

Income reliability: Can your savings support consistent monthly income?

Downside protection: What safeguards are in place to reduce losses?

Liquidity: Can you access your money if you need it?

Tax efficiency: Are you keeping more of what you earn?

Inflation protection: Will your income grow as costs rise?

Income First. Growth Second.

The most important question to ask is:

“How much income did my portfolio produce last month?”

For most Americans, the answer is zero — because their investments haven’t been structured to generate reliable income.

At FSA, we flip that model: we help you build a retirement income strategy first, then align your investments to support it — not the other way around.

The FSA Planning Approach

Using our CARES Planning Process, we help clients:

Understand their true risk exposure

Build income strategies that can withstand market volatility

Minimize taxes and optimize Social Security

Align their portfolio with real retirement goals — not average return targets